Sunday, April 26, 2026

6 min read

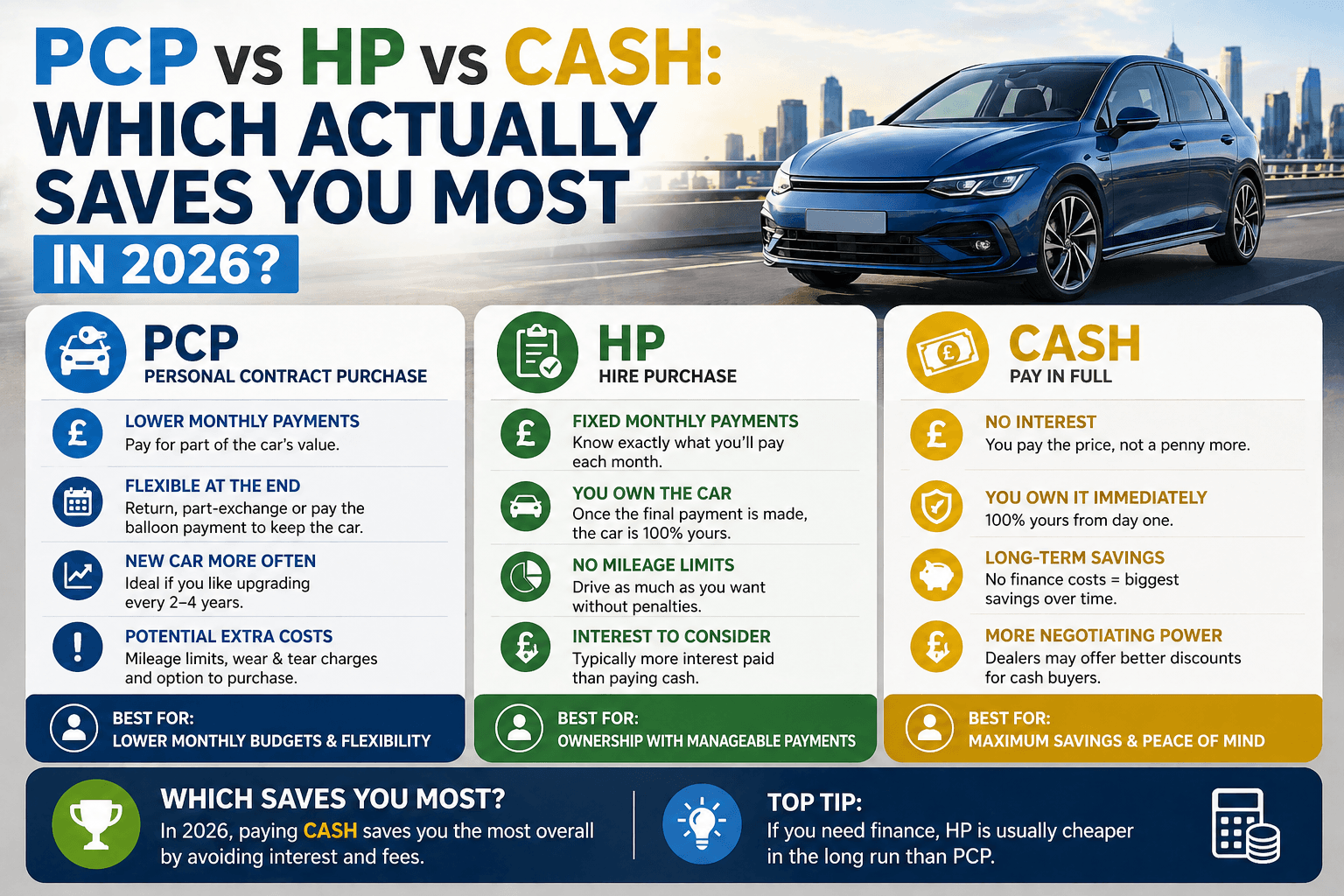

PCP vs HP vs Cash: Which Actually Saves You Most in 2026?

Quick Answer: For most buyers, paying cash is the cheapest option overall — but only if you'd genuinely have spare savings left after the purchase. HP (Hire Purchase) is usually cheaper than PCP if you intend to keep the car long-term, because PCP charges interest on the full vehicle value while you only own a portion of it. PCP is cheapest in monthly outgoings and best if you swap cars every 3–4 years. The right answer depends on what you'll do at the end of the term.

Walk into any UK dealer and you'll be offered three ways to buy a car: pay cash, take Hire Purchase (HP), or sign up to a Personal Contract Purchase (PCP). The salesperson will probably steer you toward PCP because the headline monthly figures look the lowest.

That doesn't mean PCP is the cheapest. It means it shows the smallest number on the screen. The actual total cost depends on the car, the deposit, the term, the interest rate, and — critically — what you do at the end of the agreement.

Here's how each one really works, with a worked example on a £15,000 used car.

How does paying cash for a car work?

You hand over the full purchase price in one go. The car is yours from day one. There's no interest, no monthly payment, no agreement — just ownership.

Pros:

Cheapest total cost. No interest paid.

No monthly commitment. Free up your credit file.

You own it outright — sell it whenever you want.

Cons:

Big lump sum out of your savings.

That money can't be earning interest in a savings account or ISA anymore.

If something goes wrong with the car, there's no finance company to challenge under Section 75.

How does Hire Purchase (HP) work?

You put down a deposit, then pay equal monthly instalments over an agreed term (usually 2–5 years). At the end of the term, after one final 'option to purchase' fee (typically £1–£100), the car is yours.

During the agreement, the finance company technically owns the car — but provided you keep up payments, you'll own it outright at the end. There's no mileage limit and no condition charges.

Pros:

You'll own the car outright at the end.

No mileage restrictions.

Lower interest rates than PCP, generally.

Predictable: same payment every month, full ownership at the end.

Cons:

Higher monthly payments than PCP.

You can't hand it back early without penalty (unless you've paid more than 50% under the Voluntary Termination right).

How does PCP (Personal Contract Purchase) work?

You put down a deposit, then pay smaller monthly instalments over 2–4 years. At the end of the term, you have three choices:

Pay the 'optional final payment' (the GMFV — Guaranteed Minimum Future Value) and own the car.

Hand the car back and walk away (subject to mileage and condition).

Use any equity above the GMFV as a deposit toward your next car.

The reason monthly payments are lower is simple: you're not paying off the whole car. You're paying off the difference between the purchase price and the GMFV. That GMFV chunk sits at the end as a balloon payment.

Pros:

Lowest monthly payments of the three options.

Flexibility at the end of the term.

Easy to keep upgrading to a new car every 3–4 years.

Cons:

Highest total interest cost if you keep the car long-term, because you pay interest on the full vehicle value the whole time.

Mileage limits — exceed them and you'll pay per mile (typically 7p–25p).

Condition charges — wear beyond 'fair wear and tear' costs you on hand-back.

If you want to own the car, that final balloon payment can be £6,000–£12,000 in one go.

Worked example — £15,000 used car, 4-year term

Let's run the same car three ways. Numbers are illustrative and based on typical 2026 used-car finance rates of around 10–11% APR — your actual rate will vary.

Cash:

Day 1: pay £15,000.

Total cost: £15,000.

HP — £2,000 deposit, 48 months, 10% APR:

Monthly payment: ~£330.

Final 'option to purchase' fee: ~£10.

Total paid: £2,000 + (48 × £330) + £10 = £17,850.

Total interest: £2,850.

You own the car outright.

PCP — £2,000 deposit, 48 months, 10.5% APR, GMFV £4,500:

Monthly payment: ~£250.

Total paid in monthly instalments: £2,000 + (48 × £250) = £14,000.

If you want to keep the car: pay the £4,500 GMFV. Total: £18,500. Total interest: £3,500.

If you hand the car back: total paid: £14,000. But you have no car at the end.

So if you want to own the car at the end, PCP costs £650 more than HP and £3,500 more than cash. If you want to swap cars every 4 years and hand the PCP back, you've paid £14,000 over 4 years and have nothing — versus paying £15,000 cash and having a 4-year-old car worth around £6,000–£8,000 to part-exchange or sell.

So which is actually cheapest?

Total cost, lowest to highest, for someone keeping the car:

1st — Cash: £15,000.

2nd — HP: £17,850.

3rd — PCP: £18,500.

Cash wins on total spend. Always. No interest is no interest.

But total spend isn't the only thing that matters. The right question is: which option is best for your situation?

When does PCP make more sense?

PCP genuinely is the best option if:

You like driving a newer car and intend to swap every 3–4 years anyway.

Your annual mileage is genuinely predictable and within the agreement limits.

You'd rather keep more cash in your savings or spend it elsewhere.

You want the protection of a manufacturer's warranty for the entire ownership period.

If you tick all four, PCP is the option that fits your behaviour, even if it costs more than HP on paper.

When does HP win?

HP is the better choice when:

You plan to keep the car for 5+ years.

Your mileage is high or unpredictable.

You want guaranteed ownership at the end without a big balloon payment.

You don't have the cash for an outright purchase but want the simplest, most predictable finance product.

When should you just pay cash?

Pay cash when:

You can do it without dipping below 3–6 months of emergency savings.

Interest rates on car finance (currently around 9–11%) are higher than what you'd earn on the same money in a savings account or ISA (currently around 4–5%).

You want maximum flexibility — to sell, modify or scrap the car whenever you choose.

Quick rule of thumb in 2026: if your loan APR is meaningfully higher than your savings rate, you're losing money by financing a depreciating asset. Right now, for most buyers, that means cash wins on the maths.

What about 0% finance offers?

If a manufacturer offers genuine 0% APR finance, that changes the calculation. Borrowing at 0% while keeping your cash earning 4–5% in an ISA is a clear win. Just check the offer is truly 0% and not 'representative 0%' on a tiny portion of the deal — the small print sometimes hides arrangement fees that effectively reintroduce interest.

What's the smartest play in 2026?

With current interest rates, our honest advice to most buyers is:

If you have the cash and good emergency savings: pay cash, take the discount many dealers will offer, and reinvest your monthly 'payment' into savings.

If you don't have the cash but want to own the car: HP, with the largest deposit you can comfortably afford, and the shortest term you can afford.

If you genuinely want to swap every 3–4 years: PCP, with realistic mileage limits and a clear plan for the GMFV at the end.

Whichever route you go, two non-negotiables: read the agreement before signing it, and use a finance calculator to work out the total cost — not just the monthly figure. You can check your finance eligibility with us in a couple of minutes without affecting your credit score.

Frequently Asked Questions

Is PCP a good idea?

PCP is a good idea if you want lower monthly payments and plan to swap cars every 3–4 years within the mileage limits. It's a poor idea if you intend to keep the car long-term — you'll pay more interest than on HP.

What's the cheapest way to buy a car in the UK?

Paying cash is the cheapest in pure total cost, because you pay no interest. Among finance options, HP is generally cheaper than PCP if you keep the car beyond the agreement.

Can I end a PCP agreement early?

Yes, through Voluntary Termination, once you've paid more than 50% of the total amount payable. You can also settle the agreement at any time by requesting an early settlement figure from the lender.

Does paying cash get you a better price?

Sometimes. Many dealers earn a commission from the lender on finance deals, so a cash buyer doesn't always get a better headline price. Always negotiate on the car price first, then ask about finance — not the other way around

anycolourcar Limited is registered in England and Wales under company number: 12573459. Genn Lane, Barnsley, S70 6TF. anycolourcar Limited is authorised and regulated by the Financial Conduct Authority, under FCA number: 946186. We act as a credit broker not a lender. We work with a number of carefully selected credit providers who may be able to offer you finance for your purchase. (Written Quotation available upon request). Whichever lender we introduce you to, we will typically receive commission from them (either a fixed fee or a fixed percentage of the amount you borrow) and this may or may not affect the total amount repayable. The lender will disclose this information before you enter into an agreement which only occurs with your express consent. The lenders we work with could pay commission at different rates and you will be notified of the amount we are paid before completion. All finance is subject to status and income. Terms and conditions apply. Applicants must be 18 years or over. We are only able to offer finance products from these providers. As we are a credit broker and have a commercial relationship with the lender, the introduction we make is not impartial, but we will make introductions in line with your needs, subject to your circumstances. anycolourcar Limited are registered with the Information Commissioners Office under registration number: ZA863807

Showroom: The Old Garage, Genn Lane, Worsbrough, Barnsley, S70 6TF.

Service Centre: Stairfoot Business Park, Bleachcroft Way, S70 3PA

- hello@anycolourcar.com

- Customer Carecustomer@anycolourcar.com

- Monday

- Tuesday

- Wednesday

- Thursday

- Friday

- Saturday

- Sunday

- 09:00 - 18:00

- 09:00 - 18:00

- 09:00 - 18:00

- 09:00 - 18:00

- 09:00 - 18:00

- 09:00 - 17:00

- CLOSED

2026 anycolourcar.com. All rights reserved

Powered by Motorsales.ai - Innovating the future of car sales